FINANCIAL COACHING ENGAGEMENT FRAMEWORK

The following question often pops up in conversations around financial coaching: Do I always have to engage in a formal coaching process that consists of multiple sessions?

We will explore the question by looping back to our conversations over the past few weeks and then expanding.

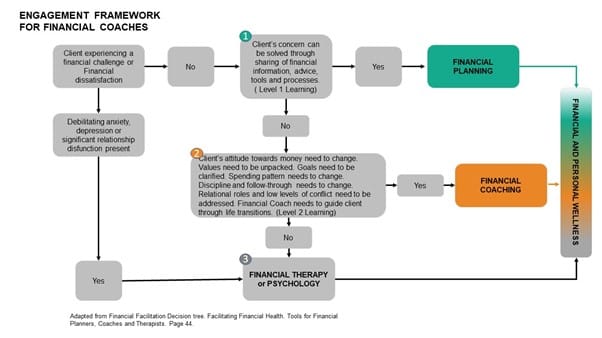

In Facilitating Financial Health, Tools for Financial Planners, Coaches and Therapists, the authors share a financial facilitation decision tree that I adapted to align to the Ontological Coaching model.

With reference to the diagram, we can see that we engage with a client and are experiencing a specific challenge that they voice to us. We ask a few questions and assess that (diagram point 1) client concerns can be solved by sharing financial information, advice, tools, or new processes. For example, clients only need factual information or a product to address their concerns or need. As discussed last week, this is level 1 learning.

The alternative can be that we assess our client needs to:

- Change their attitude towards money,

- Align their values, meaning and money,

- Build the competency to manage their money,

- Plan for a significant life transition, and

- Aid them when they are experiencing a major life transition.

All of the above are examples where most clients will need to change their structure of interpretation or require new skills.

We now know we need to explore their way of being, to enable level 2 learning (diagram point 2). As the client needs to broaden their language, adopt a mood that will support them and embody a new way of observing the world to deal with the concern or challenges.

It is also important to note that when our client is experiencing debilitating anxiety or significant relationship dysfunction, it is our ethical responsibility to refer them to a therapist or psychologist (diagram point 3). Secondly, suppose we cannot support our client either due to differences in values or personality, as examples. In that case, it is also our responsibility to refer the client to another financial coach or planner.

Back to level 2 (diagram point 2) learning, we need to perform certain types of engagements to support our clients to change how they observe and address their concerns or challenges. Let’s see how we can approach these engagements.

TYPES OF COACHING ENGAGEMENTS

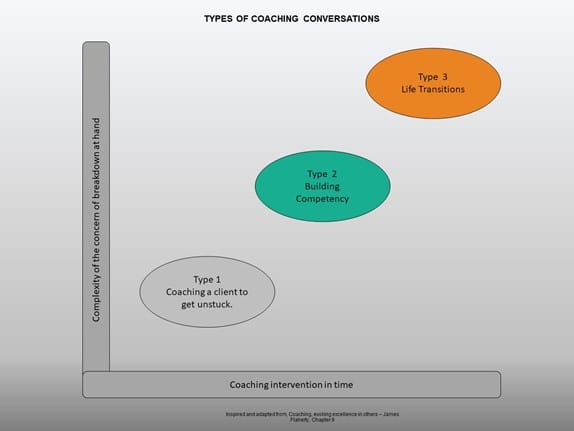

James Flaherty shares three types of coaching conversations in his book, Coaching, evoking excellence in others, and we will use his model as a distinction for our discussion.

He shares the following quote in the introduction to the chapter that is very relevant to coaching:

“He has to see on his own behalf and in his own way the relations between means and methods employed and results achieved. Nobody else can see for him, and he can’t see just by being ‘told’, although the right kind of telling may guide his seeing and thus help him to see what he needs to see” – John Dewey (Flaherty, 2005, p. 125)

The quote re-iterates the approach that the quality of conversations will determine the quality of our coaching conversations. The quality of our coaching conversations can be assessed by the awareness we create with our clients, and the new action the client will take, to lead a more joyous life with less suffering.

On the vertical axis, we have the complexity of the concern or breakdown of our client. If we view complexity from a financial coaching perspective, we can also say how ingrained the breakdown is, and how it became a part of the client’s way of coping with life over the years. On the other hand, complexity could also be that life happens, for example, the client unexpectedly gets retrenched, and their identity is their job. They now need to deal with the change, find themselves and recreate a new life of meaning.

On the horizontal axis, we have the intervention time we will spend with the client to coach the client on the concern or breakdown.

TYPE 1 – IMPROMTO FINANCIAL COACHING

Impromptu coaching will generally show up in our conversation with a client, colleague, or employee. We will then, at the moment, use our coaching skills and, with permission, explore what we are observing and how it is serving the client, using parts of the 10-Step Coaching Process that applies to the situation.

The following is some examples:

- The client is making some assessments based on generalisations about investment returns and the best funds in the market.

- The client is continuously complaining about life in general.

- The client is struggling to take action based on a request. An example could be providing specific information required for the FNA or executing the plan.

TYPE 2 – COACHING FOR FINANCIAL COMPETENCY

Our engagements with the client indicate that they want to build a specific competency, a new way of being to enable them to be more effective in building prosperity or life a better lifestyle. These coaching interventions will typically be structured over some time, say six months.

The following is some examples:

- The client battle to stay within budget.

- Couples have conflicts around managing their finances and their roles in managing their finances. This is a good example, where depending on the challenge, it could require either type 1,2, or 3 coaching or therapy.

- The client uses long-term savings to fund a short-term lifestyle.

TYPE 3 – LIFE TRANSITIONS

This coaching typically originates either from being pro-active and planning for certain life transitions or life happens, and the client needs to deal with the life transition all of a sudden.

The following are some examples:

- The client wants to start a side hustle

- The client just heard they are retrenched

- The client needs to retire in five years.

- The client’s partner just passed away.

Bibliography

Flaherty, J., 2005. Coaching, Evoking excellence in others. 2005 red. Burlington: Elsevier.

Klontz, B., Kahler, R. & Klontz, T., 2016. Facilitating Financial Health, Tools for Financial Planners, Coaches and Therapists. 2nd red. Erlanger: The National Underwriter Company.