Financial Wellbein, beyond the numbers.

A conversation with Marius van der Merwe, CEO of Amity Investment Solutions, had me thinking. We were unpacking his Financial Wellbeing Model, and somewhere in that conversation I found myself asking a different question entirely. Not “what does financial wellbeing look like on a spreadsheet?” but rather, “how does it show up in someone’s way of being, in how they see themselves and the world?” This is my first stab at answering that.

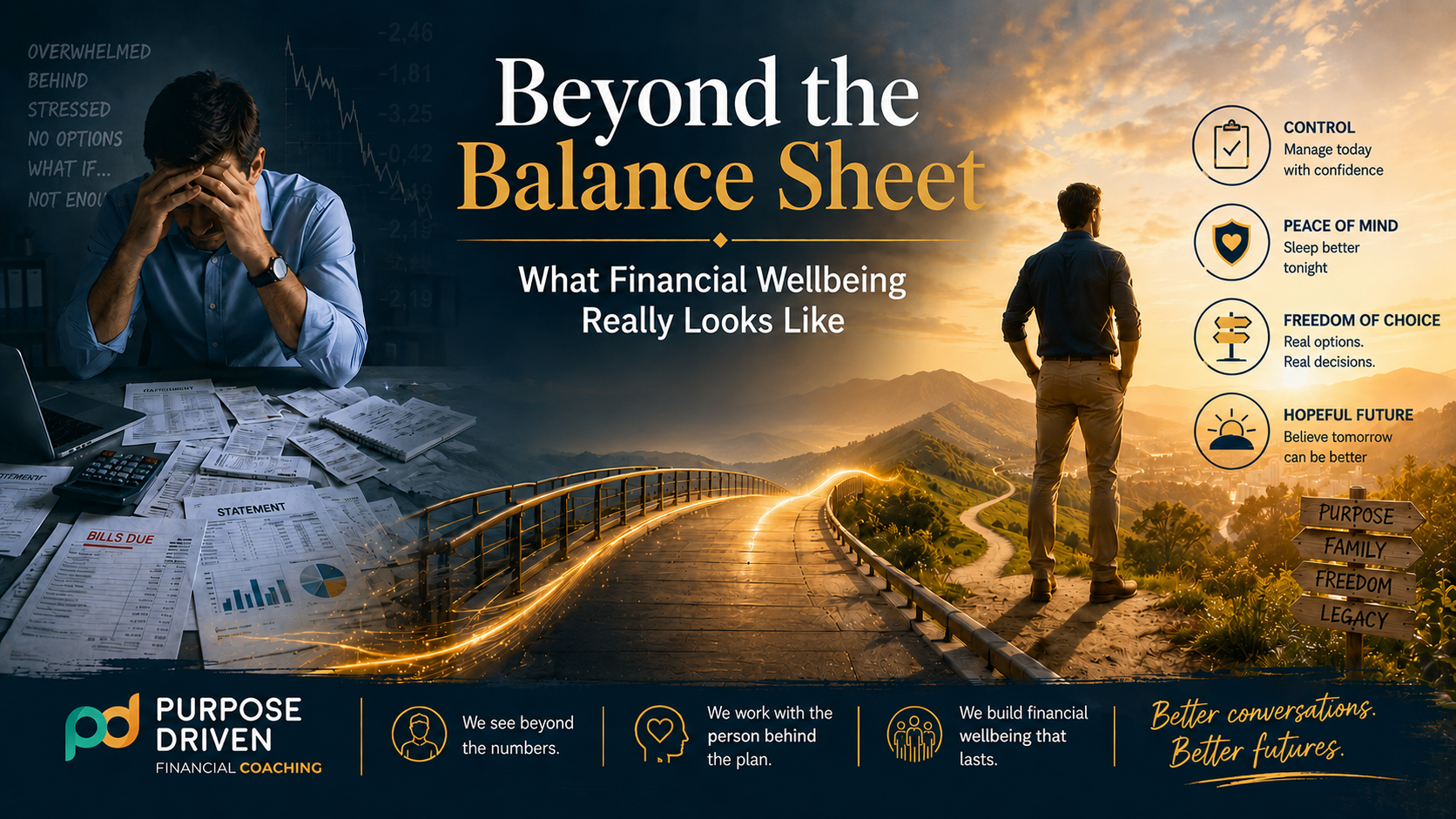

What is financial wellbeing, and why does it matter for South Africans?

Financial wellbeing goes far beyond how much money someone has. Marius van der Merwe defines it as the perception a person has of being able to sustain their current standard of living, while feeling they are making progress toward a desired future, with the freedom to enjoy life along the way.

That distinction matters enormously in the South African context, where two households earning similar incomes can experience their financial lives in completely different ways. One feels in control and hopeful. The other feels trapped and anxious. The difference is rarely just the numbers. It’s the relationship the person has with their money, and with themselves.

As a financial coach and trainer, I see this constantly. We’re brilliant at diagnosing what’s wrong with a financial plan. What we’re less practiced at is reading the person sitting across from us.

What are the four pillars of financial wellbeing?

Van der Merwe’s model identifies four cornerstones that together determine a client’s financial wellbeing experience:

Control refers to the ability to manage day-to-day finances: meeting obligations, managing debt, and knowing where the money goes.

Peace of Mind reflects reduced financial anxiety, adequate protection, and the confidence that a financial shock won’t be catastrophic.

Freedom of Choice speaks to having genuine options in life, the ability to change jobs, fund experiences, or simply say no to things that don’t serve you.

A Hopeful Future is the belief that tomorrow can actually be better, grounded in progress toward meaningful goals and a sense of financial direction.

These four pillars are not just financial measures. They are expressions of how someone is living with money. And that inner experience is what financial coaching is designed to shift.

How does financial wellbeing show up in a client’s way of being?

This is where ontological coaching offers something that traditional financial planning doesn’t.

In ontological coaching, we work from a foundational premise: we don’t see the world as it is. We see the world as we are. Our way of being, shaped through the language we use, the moods we carry, and how we hold ourselves in our bodies, creates the lens through which we interpret our financial reality.

Each of the four wellbeing pillars has a healthy and an unhealthy way of being attached to it.

When Control is present, clients are grounded, agentic, and organised. When it’s absent, they become avoidant, overwhelmed, and resigned. A client who says “I’ve never been good with money” isn’t just reporting a skills gap. They’re expressing an identity, and that identity drives their behaviour far more than any budgeting tool ever will.

When Peace of Mind is present, clients feel prepared and trusting. When it’s absent, they become hypervigilant, catastrophising, and defensive. Peace of mind, seen through an ontological lens, is not only built by having the right insurance policy. It’s also an inner relationship with uncertainty, and that relationship can be coached.

When Freedom of Choice is present, clients feel empowered and creative. When it’s absent, they become passive, cynical, and dependent. The language of helplessness, “I have no choice,” “I’m stuck,” is not just a mindset. It’s a mood that closes down creative thinking entirely.

When Hopeful Future is present, clients are visionary and purposefully committed. When it’s absent, they drift toward despair and survivalism. Without hope, financial planning becomes compliance. With it, planning becomes transformation.

What are the enemies of learning in financial wellbeing coaching?

Every wellbeing dimension has what we call enemies of learning: the moods and language patterns that keep clients locked in familiar, unhelpful loops.

For Control, the enemy is resignation. “I’ll never catch up. What’s the point?” For Peace of Mind, it’s fear and catastrophising. “What if everything goes wrong?” For Freedom of Choice, it’s helplessness and cynicism. “There’s no way out.” For Hopeful Future, it’s despair and drift. “Things never change for people like me.”

These are not character flaws. They are interpretations of reality. And interpretations can shift, but only when we create the conditions for that shift to happen. That is the work of financial coaching.

What are the allies of learning that financial coaches can cultivate?

The allies of learning are the moods and dispositions that open clients to change: curiosity, humility, courage, trust, ambition, and the willingness to sit with discomfort long enough to find out what’s actually in the way.

As financial coaches, our role is partly to create the conversational conditions where these allies can emerge. That means listening for what’s beneath the presenting concern. It means asking questions that open reflection rather than close it. It means not rushing to solutions before we’ve understood the person.

How can financial coaches use the wellbeing model in practice?

Here is a practical framework for weaving the Financial Wellbeing Model into your client engagement process, especially in discovery conversations and annual reviews.

Step one: Notice mood and language before facts. When a client talks about money, what mood do you hear? Resignation? Fear? Frustration? Hope? That mood is data, and it tells you more about what kind of coaching is needed than any cashflow statement.

Step two: Explore the structure of interpretation underneath. Ask gently: “What do you believe about this situation?” “How long have you held that view?” “Is that belief still serving you?” You’re not doing therapy. You’re doing coaching. But you’re listening at a level that most financial conversations never reach.

Step three: Distinguish the facts from the story. Once you’ve identified the interpretation, help the client separate what is objectively true from the meaning they’re making of it. That distinction alone can be profoundly liberating.

Step four: Introduce first-order practices. This is where the tools, habits, and behaviours come in: a weekly cashflow review, a simple emergency fund milestone, a 10-minute monthly financial check-in ritual, a protection review with clear coverage targets. These practices matter. But they land differently, and stick far more reliably, when the client has first shifted something in how they see themselves and their situation. The tool without the inner shift rarely holds.

What questions should financial coaches hold in client conversations?

Before your next client meeting, try carrying these four questions into the room:

Does this client feel in control of their day-to-day financial life? Do they have peace of mind, or are they quietly bracing for the worst? Do they feel like they have genuine options, or do they feel financially trapped? And do they genuinely believe their future can be different?

You may not ask these questions directly. But if you’re listening for the answers, you’ll hear them. They show up in how clients speak about money, about the future, and about themselves.

How does this model shift the way financial planners and coaches add value?

As Marius van der Merwe puts it, the future of advice lies in broadening our value proposition to include the subjective dimensions of financial wellbeing. Instead of measuring success only by returns, we begin measuring it by the confidence our advice gives clients, the peace of mind they experience, the freedom they have to enjoy life, and the hope financial planning provides for their desired future.

For coaches, this is also an invitation to honest self-reflection. Are we in information-delivery mode, or are we genuinely listening for the way of being that’s shaping our client’s relationship with their financial life? That shift from product-first to wellbeing-first requires us to become different kinds of observers. And that’s a practice, not a once-off decision.

What is the deeper purpose of financial wellbeing coaching?

Marius’s model reminded me of something I believe deeply: financial wellbeing is less about how much money someone has and more about how they’re living with what they have.

It’s the difference between a client who earns well and feels trapped, and a client with modest means who feels genuinely free and hopeful. Our work, at its best, is the work of expanding that inner experience.

Not just better plans. Better observers. Better relationships with money, with the future, and with themselves.

That, to me, is what purpose-driven financial coaching is really about.

References

Van der Merwe, M. (2026). From wealth to wellbeing: helping clients thrive, not just survive. Blue Chip Digital, Issue 97. Amity Investment Solutions. https://bluechipdigital.co.za/featured/from-wealth-to-wellbeing-helping-clients-thrive-not-just-survive/

Crafford, H. (2022). Purpose-Driven Financial Coaching. Craffies Coaching.

Sieler, A. (2003). Coaching to the Human Soul: Ontological coaching and deep change (Vol. 1). Newfield Institute.

Sieler, A. (2007). Coaching to the Human Soul: Ontological coaching and deep change (Vol. 2). Newfield Institute.

Prawitz, A.D. & Cohart, J. (2016). Financial management competency: Financial resources, locus of control and financial wellness. Journal of Financial Counseling and Planning, 27(2), 142–157.

BREAKDOWNS IS A CALL TO ACTION

INTRODUCTION Breakdowns, viewed through the lens of ontology as expounded by the influential philosopher Martin Heidegger, represent a profound philosophical exploration of human experience. Heidegger's ontology delves into the nature of being and how individuals...

How Financial Coaches Can Support Clients to Transform Negative Money Assessments into Positive Mindsets

Introduction In the realm of financial coaching, understanding the psychology of money is paramount. Clients often come with myriad financial assessments that can empower or hinder their financial journey. These assessments, formed through linguistic processes of...

Empowering Financial Change: Harnessing Motivational Interviewing in Coaching

As financial coaches and planners, incorporating MI into our practice can provide valuable support to clients in overcoming challenges and developing new strategies. This article explores the essence of Motivational Interviewing and its relevance in financial coaching.

8 PERSONAL FINANCE BOOKS YOU MUST READ

When it comes to personal finance, knowledge is power. Educating yourself about money management and investing can significantly impact your financial well-being. To help you on your journey, I have compiled eight must-read books covering various aspects of personal...

Why understanding our clients’ values and purpose is essential before we draft a financial plan?

Values can have a significant influence on an individual's purpose. An individual's purpose often reflects their deeply held values and beliefs, as it is shaped by what they consider most important in life. For example, if an individual values creativity, they may...

What is your client’s communication preference?

As financial coaches and planners, it is vital to understand our clients preferred communication styles. Our clients’ communication preferences will influence how we communicate with them and present information. Furthermore, it gives us an indication of how they may...

FINANCIAL POWER IN LANGUAGE

How we see the world is determined by the language we use, the mood we embody, and our bodies. In this article, we will explore how language create our reality of Financial Prosperity.

ACCELERATING FINANCIAL WELLNESS

The following question often pops up in conversations around financial coaching: Do I always have to engage in a formal coaching process that consists of multiple sessions?

FINANCIAL COACHING AS A CATALYST FOR NEW POSSIBILITIES

As financial coaches we see clients seek our services when they are experiencing some or other challenge and/or concerns that they cannot solve or see new possibilities for. For example, they get retrenched or battle to make ends meet.

INTEGRATION BETWEEN FINANCIAL COACHING AND FINANCIAL PLANNING

10 Points of Integration between Financial Coaching and Financial Planning